The wealth life cycle is broken into two main phases: accumulation and distribution.

Wealth Accumulation - It is our experience that the accumulation is the easier part. You save money, set accurate budget and wealth accumulation targets, expect inflation, and use stocks to stay ahead.

Wealth Distribution - The distribution phase is where it gets difficult. This is primarily because of taxes. Taxes for you, taxes for your spouse, and taxes for your heirs. While we want you to have confidence you will achieve your accumulation goals, we also want to proactively assess how to minimize your taxes in the distribution phase of the wealth life cycle. We focus on utilizing our wealth management process to increase your after-tax wealth and help you and your spouse avoid mistakes that cost you money.

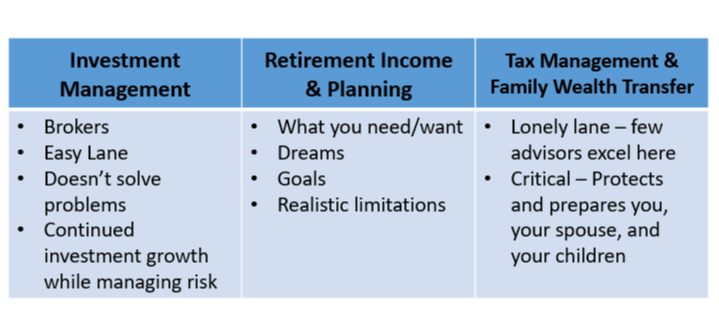

Our Three Lanes of Focus

Who can you trust to give you unbiased investment advice?

If you are like most people, you assume that someone who provides investment advice to you must be required to act in your best interests. Unfortunately, that’s only true for some advisors – those who are fiduciaries like us. Registered Investment Advisers are legally obligated to place your interests first. They are fiduciaries. That means they must not only be loyal to serving your exclusive best interests, they also must adhere to a high standard of professional competence.